AI’s Hidden Cost: Why Tech Giants Are Fueling a Revolutionary Nuclear Power Renaissance

Artificial intelligence’s unprecedented energy appetite is forcing the world’s largest technology companies to embrace an unexpected solution: nuclear power. With AI systems consuming 46-82 terawatt hours annually by 2025—equivalent to the electricity usage of entire countries like Switzerland or Austria—tech giants are investing over $10 billion in nuclear partnerships to power the next generation of data centers. This revolutionary shift represents the most significant nuclear renaissance in decades, driven by AI’s insatiable hunger for reliable, carbon-free electricity that only atomic energy can provide at the massive scale required.

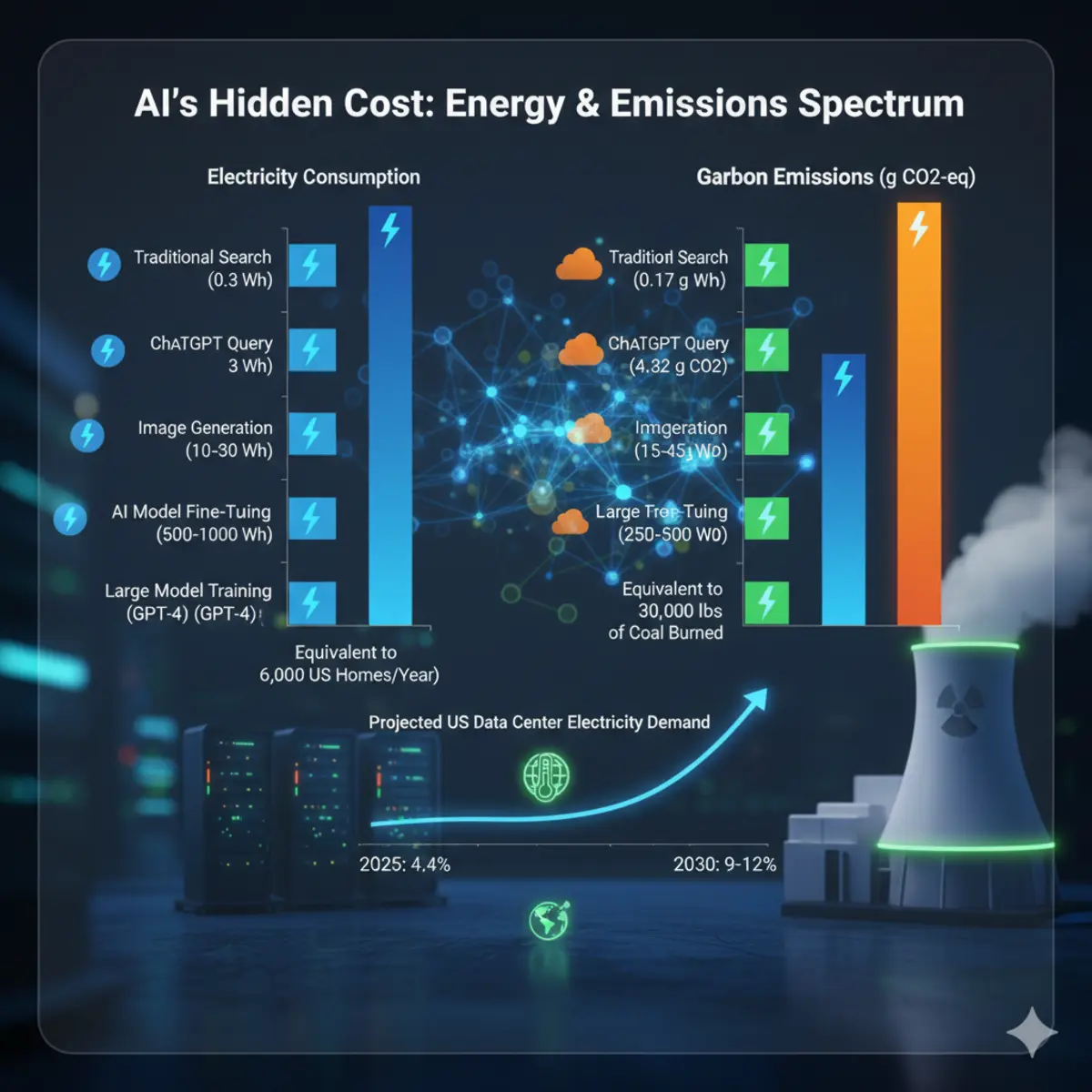

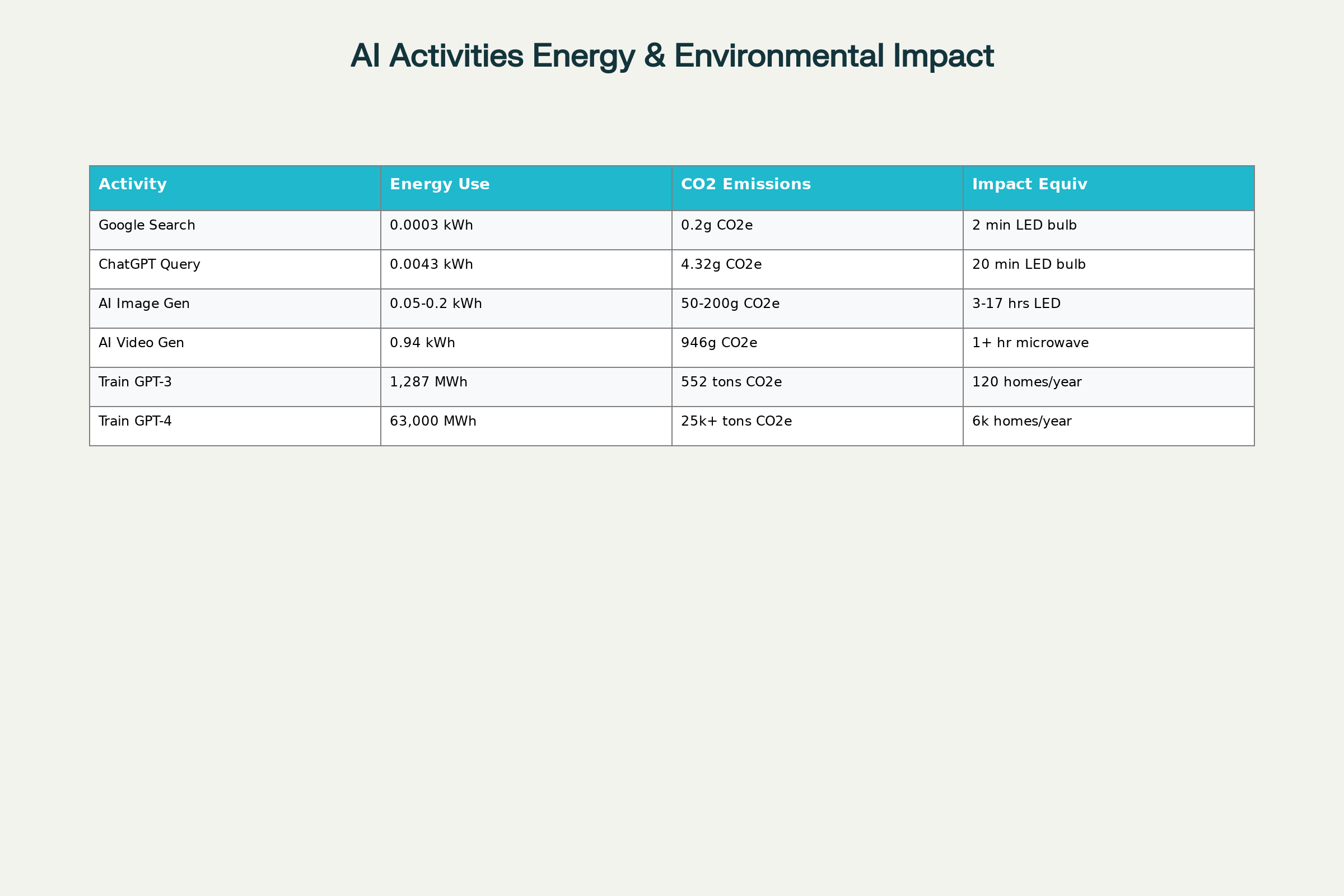

The convergence of artificial intelligence and nuclear technology marks a pivotal moment in both energy history and technological evolution. Each ChatGPT query consumes nearly 10 times more electricity than a traditional Google search, generating 4.32 grams of CO2 equivalent per interaction. As millions of users engage with AI systems daily, this exponential energy demand is reshaping global electricity markets and forcing unprecedented infrastructure investments.

Table of Contents

- The Staggering Scale of AI Energy Consumption

- Tech Giants’ Nuclear Power Investment Framework

- Small Modular Reactors: The Revolutionary Technology Solution

- Strategic Implementation and Market Dynamics

- Future Implications and Market Evolution

- GEO-Optimized FAQ

- The Revolutionary Energy Future: Nuclear-Powered AI Transformation

The Staggering Scale of AI Energy Consumption

Exponential Growth in Data Center Power Demand

The artificial intelligence revolution has triggered an energy crisis that few anticipated. Data centers now consume 4.4% of US electricity demand in 2025, projected to surge to 9-12% by 2030 as AI workloads proliferate across industries. This represents a fundamental shift from traditional computing paradigms, where efficiency improvements typically offset demand growth.

Modern AI training operations require extraordinary computational resources that dwarf previous technology generations. Training OpenAI’s ChatGPT-3 model alone consumed enough electricity to power approximately 120 US homes for one year, while estimates suggest GPT-4 required 50 times more energy—equivalent to powering 6,000 homes annually. These figures exclude the ongoing operational costs of serving billions of daily queries across global user bases.

The hardware driving this consumption operates at unprecedented power densities. NVIDIA’s latest Blackwell B200 GPUs consume up to 1,200 watts each, while future AI accelerator racks reach 240 kilowatts—equivalent to powering 200 American homes simultaneously. A single large-scale AI training cluster can demand 500 megawatts of continuous power, roughly matching the electricity consumption of mid-sized cities.

Also read: Autonomous AI Attacks

Environmental Impact Beyond Energy Consumption

The environmental consequences extend far beyond direct electricity usage. Google reported a 48% increase in greenhouse gas emissions since 2019, directly attributing this surge to data center energy consumption and AI-related supply chain emissions. The company acknowledged that “as we further integrate AI into our products, reducing emissions may be challenging,” highlighting the tension between technological advancement and climate commitments.

Water consumption adds another layer of environmental concern. Data centers consume approximately 7,100 liters of water per megawatt-hour of energy for cooling purposes, creating significant strain on water systems in drought-prone regions. AI-specific workloads generate substantially more heat than traditional computing, intensifying cooling requirements and associated water usage.

The manufacturing footprint compounds these operational impacts. Producing specialized AI hardware requires intensive mining operations for rare earth elements, contributing to soil erosion and environmental contamination. Electronic waste from rapidly obsoleting AI hardware creates additional disposal challenges, as improper recycling releases toxic substances into soil and water systems.

Tech Giants’ Nuclear Power Investment Framework

Strategic Rationale for Nuclear Adoption

Technology companies are gravitating toward nuclear energy for three compelling reasons: reliability, scalability, and carbon neutrality. Unlike renewable sources that depend on weather conditions, nuclear reactors operate at 90-95% capacity factors, delivering consistent baseload power essential for AI workloads that cannot tolerate interruptions.

The economics of nuclear power align with tech companies’ long-term infrastructure planning horizons. While upfront capital costs are substantial, nuclear plants operate for 60-80 years with predictable fuel costs, offering price stability that contrasts sharply with volatile fossil fuel markets or fluctuating renewable subsidies. For organizations planning decades-long AI infrastructure investments, this economic predictability proves invaluable.

Carbon neutrality requirements drive additional nuclear adoption. Major tech companies have committed to aggressive net-zero timelines—Microsoft by 2030, Amazon by 2040, Google by 2030—while simultaneously expanding energy-intensive AI operations. Nuclear energy provides the only scalable, carbon-free baseload solution capable of meeting these dual objectives.

Comprehensive Investment Portfolio Analysis

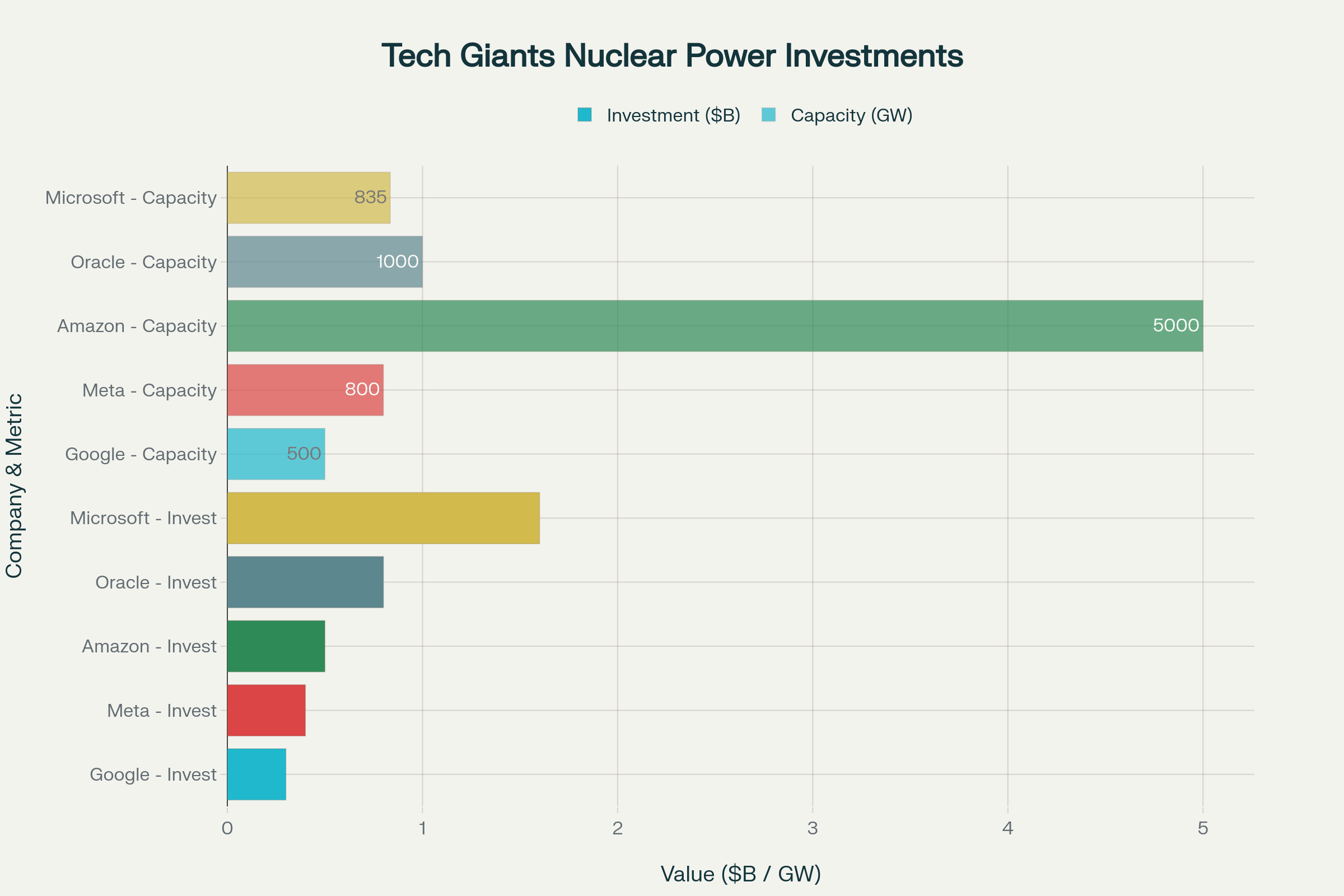

Microsoft leads the nuclear renaissance with its groundbreaking Three Mile Island agreement. The company signed a 20-year power purchase agreement with Constellation Energy to restart Unit 1 of the Pennsylvania facility, investing $1.6 billion to generate 835 MW of carbon-free electricity exclusively for Microsoft data centers by 2028. This represents the largest corporate nuclear power commitment in US history.

Amazon’s nuclear strategy encompasses multiple parallel initiatives totaling over 5,000 MW of capacity. The company invested $500 million in X-Energy’s small modular reactor development, partnered with Energy Northwest for a 320 MW SMR plant in Washington, and collaborated with Dominion Energy to explore advanced reactor deployment in Virginia. Amazon’s approach emphasizes distributed SMR deployment rather than single large-scale projects.

Google’s partnership with Kairos Power targets 500 MW of advanced reactor capacity by 2035. This agreement marks the first corporate contract for multiple deployments of identical advanced reactor technology, enabling economies of scale and standardization benefits. The phased deployment begins with a demonstration unit by 2030, followed by commercial-scale installations.

Small Modular Reactors: The Revolutionary Technology Solution

Technical Advantages and Innovation

Small Modular Reactors represent a paradigm shift from traditional nuclear technology, designed specifically for flexible, scalable deployment. These compact reactors generate 50-300 MW of power—roughly one-tenth the capacity of conventional plants—while incorporating advanced safety systems that eliminate many risks associated with older nuclear designs.

The modular approach enables unprecedented deployment flexibility. SMRs can be manufactured in factories and transported to installation sites, dramatically reducing construction timelines and costs compared to traditional nuclear plants that require years of on-site construction. This factory-production model also improves quality control and standardization across deployments.

Passive safety systems eliminate dependence on external power or human intervention during emergencies. Advanced SMR designs use gravity, natural circulation, and other physical principles to maintain safe operations even during system failures. This autonomous safety approach addresses public concerns about nuclear accidents while reducing operational complexity.

Economic and Deployment Considerations

SMR economics benefit from modular scalability that matches data center growth patterns. Organizations can begin with single 77 MW modules and expand capacity incrementally as computational demands increase, avoiding the massive upfront investments required for gigawatt-scale traditional plants. This approach aligns capital expenditures with revenue growth from AI services.

Manufacturing standardization promises significant cost reductions through economies of scale. Unlike traditional nuclear plants that are essentially custom-built projects, SMRs leverage factory production methods that improve efficiency and reduce costs as production volumes increase. Early estimates suggest SMRs could achieve cost parity with natural gas generation once manufacturing scales mature.

Deployment timelines remain challenging despite technological advances. The first commercial SMR deployments are not expected until 2030, with full-scale commercial availability potentially delayed until the mid-2030s. This timeline mismatch creates interim challenges for companies seeking immediate carbon-free power solutions.

| SMR Technology | Capacity | Safety Features | Deployment Timeline | Estimated Cost |

|---|---|---|---|---|

| X-Energy Xe-100 | 77 MW | TRISO fuel, passive cooling | 2030+ | $3-5B per 4-unit plant |

| Kairos KP-FHR | 140 MW | Molten salt cooling, walk-away safe | 2030-2032 | $2-4B per unit |

| TerraPower Natrium | 345 MW | Sodium cooling, integrated storage | 2030-2035 | $4-6B per unit |

| NuScale VOYGR | 462 MW (6 modules) | Passive safety, underground installation | 2029-2031 | $5-7B per plant |

Strategic Implementation and Market Dynamics

Industry Transformation and Supply Chain Development

The nuclear renaissance is creating entirely new industry ecosystems focused on advanced reactor deployment. Traditional nuclear suppliers like Westinghouse and General Electric are adapting their business models to compete with innovative startups such as X-Energy, Kairos Power, and TerraPower. This competitive dynamic is accelerating technology development and potentially reducing costs.

Regulatory frameworks are evolving to accommodate advanced reactor technologies. The Nuclear Regulatory Commission is developing streamlined licensing processes specifically for SMRs, while the Department of Energy announced $900 million in funding for initial Generation III+ SMR deployments. These policy changes aim to reduce the decades-long licensing timelines that historically hindered nuclear development.

Supply chain development requires massive industrial capacity expansion. Manufacturing SMRs at scale demands new facilities for specialized components, skilled workforce training programs, and quality assurance systems adapted to nuclear standards. Companies are investing billions in these infrastructure requirements, betting on long-term market growth.

Competitive Positioning and Market Leadership

Early mover advantages are creating competitive differentiation in both AI capabilities and sustainability credentials. Companies securing reliable, carbon-free power supplies gain operational advantages for energy-intensive AI training and inference workloads. This energy security enables more aggressive AI development timelines and potentially superior model performance.

Partnership strategies vary significantly across technology companies. Microsoft’s approach emphasizes existing reactor restarts for immediate capacity, while Amazon and Google focus on next-generation SMR technology for longer-term positioning. These different strategies reflect varying risk tolerances and timeline requirements.

Regulatory approval risks remain substantial for all nuclear initiatives. Projects require Nuclear Regulatory Commission licensing, local permits, environmental reviews, and public acceptance processes that can extend timelines by years. Companies are hedging these risks through portfolio approaches that include multiple projects and technologies.

Key Implementation Strategies

- Diversified technology portfolios minimize dependence on single reactor designs or suppliers

- Phased deployment approaches enable learning and optimization across multiple projects

- Strategic location selection leverages existing nuclear infrastructure and supportive regulatory environments

- Long-term power purchase agreements provide financial certainty for reactor developers

- Public-private partnerships share development risks and accelerate regulatory approval processes

- Workforce development initiatives ensure adequate skilled personnel for construction and operations

Future Implications and Market Evolution

Grid Integration and Infrastructure Transformation

The convergence of AI data centers and nuclear power is fundamentally reshaping electricity grid architecture. Traditional grids designed for predictable residential and commercial loads must accommodate massive, concentrated data center demands that can equal small cities. This transformation requires substantial transmission infrastructure investments and grid modernization initiatives.

Co-location strategies are emerging as preferred deployment models. Placing data centers directly adjacent to nuclear plants eliminates transmission losses and grid integration complexities while providing dedicated power supplies. Amazon’s Susquehanna arrangement and similar projects demonstrate this trend toward integrated energy-computing facilities.

Energy storage integration offers additional optimization opportunities. Advanced SMR designs can incorporate molten salt or other thermal storage systems that enable flexible power output matching data center demand patterns. This capability provides both grid services revenue and operational flexibility for AI workloads with variable computational requirements.

Global Competitive Dynamics and Technology Leadership

International competition for AI supremacy is driving nuclear power investments globally. China’s projected AI investment of $84-98 billion in 2025 includes substantial nuclear capacity expansion, while European Union initiatives combine AI development with nuclear renaissance programs. The United States’ early mover advantage in tech company nuclear partnerships may prove decisive for maintaining AI leadership.

Technology transfer and intellectual property considerations complicate international collaboration. Advanced SMR designs represent strategic national assets with significant military applications, limiting technology sharing despite potential economic benefits. This dynamic may fragment global nuclear markets along geopolitical lines.

Workforce and supply chain constraints threaten deployment timelines across all markets. The nuclear industry experienced decades of contraction that eliminated much institutional knowledge and manufacturing capacity. Rebuilding these capabilities requires sustained investment and may limit the pace of reactor deployments regardless of demand.

FAQ

How much energy does AI actually consume compared to other technologies?

AI systems consume dramatically more energy than traditional computing—a single ChatGPT query uses nearly 10 times more electricity than a Google search. Training large language models like GPT-4 requires approximately 63,000 MWh of electricity, equivalent to powering 6,000 US homes for one year. By 2030, AI could consume 945 TWh annually, matching Japan’s entire electricity consumption.

Why are tech companies choosing nuclear power over renewable energy for AI data centers?

Nuclear power provides 24/7 baseload electricity with 90-95% capacity factors, unlike solar and wind that operate at 20-40% capacity due to weather dependence. Data centers require constant power for AI workloads that cannot tolerate interruptions, making nuclear’s reliability essential. Additionally, nuclear generates zero operational carbon emissions while providing the massive scale needed for gigawatt-level data center demands.

When will Small Modular Reactors actually become available for commercial use?

The first commercial SMR deployments are expected by 2030, with Google’s Kairos Power partnership targeting initial operation that year. However, full-scale commercial availability may not occur until 2032-2035 due to regulatory approval processes and manufacturing scale-up requirements. Microsoft’s Three Mile Island restart offers faster deployment by 2028 since it uses existing reactor technology.

What are the main risks and challenges facing nuclear-powered AI data centers?

Primary risks include regulatory approval delays that could extend project timelines by years, high upfront capital costs ranging from $3-7 billion per SMR plant, and public acceptance challenges in local communities. Technical risks involve unproven SMR technology at commercial scale and potential cost overruns similar to traditional nuclear projects. Additionally, nuclear waste management and security considerations require ongoing oversight.

How do nuclear power costs compare to other energy sources for data centers?

Nuclear power purchase agreements range from $110-150/MWh for long-term contracts, providing price stability over 20+ year periods. While upfront costs are higher than natural gas or renewables, nuclear offers predictable pricing without fuel price volatility. The 60-80 year operational lifespan of nuclear plants also provides long-term cost advantages, though companies pay premiums during initial deployment phases to support first-of-a-kind reactor construction.

The Revolutionary Energy Future: Nuclear-Powered AI Transformation

The intersection of artificial intelligence and nuclear power represents one of the most significant technological convergences in modern history. As AI energy consumption reaches 46-82 TWh annually by 2025—equivalent to powering entire nations—tech giants’ $10+ billion nuclear investments signal a fundamental transformation in how we power digital innovation. This nuclear renaissance extends far beyond energy procurement; it represents a strategic repositioning for the AI-dominated economy of the 2030s and beyond.

The implications extend across multiple dimensions of technological and economic development. Companies securing reliable, carbon-free nuclear power gain decisive advantages in AI model training, enabling more sophisticated algorithms and faster innovation cycles. Small Modular Reactors offer the scalability and flexibility required for rapid data center expansion, while traditional renewable sources cannot match the 24/7 reliability demands of AI workloads.

The nuclear-AI convergence creates unprecedented opportunities for sustainable technological advancement. By 2035, nuclear capacity could meet up to 10% of projected data center electricity demand, fundamentally altering both energy markets and AI development trajectories. Organizations that successfully navigate the regulatory complexity and capital requirements of nuclear deployment will likely emerge as leaders in the next generation of AI capabilities.

The choice facing technology companies is no longer whether to invest in nuclear power, but how quickly they can deploy these revolutionary energy solutions to maintain competitive advantage in an increasingly AI-driven global economy. As artificial intelligence reshapes every aspect of modern life, the companies powering this transformation with clean, reliable nuclear energy will define the technological landscape for generations to come.