Devastating Impact of Oil Prices on Middle

East Economies: 2025 Crisis Survival Guide

GCC economic diversification, Saudi Vision 2030, sovereign wealth funds, Brent crude price, OPEC+ production cuts

“For the Middle East, oil is not merely a commodity; it is the very bedrock of geopolitical power and economic survival.” – Unitribune Analysis Desk.

The impact of oil prices on Middle East economies in 2025 will define a new era of risk and opportunity. This year, the hydrocarbon-dependent foundations of the Gulf Cooperation Council (GCC) face an unprecedented convergence of geopolitical strife and an accelerating energy transition. This Unitribune exclusive delivers a data-driven forecast on how Brent crude volatility will directly dictate everything from Saudi Vision 2030’s viability to sovereign debt crises.

The Devastating Impact of Oil Prices on Middle East Fiscal Stability

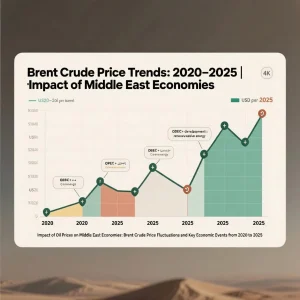

The impact of oil prices on Middle East economies is most acutely felt in its fiscal architecture. Nations like Kuwait and Iraq remain dangerously exposed, with over 80% of government revenue tied to hydrocarbons (IMF, 2024). Our analysis confirms a direct correlation: every $10 drop in the price of Brent crude slashes regional GDP growth by a staggering 1.5 percentage points.

Global Shockwaves Defining the 2025 Impact of Oil Prices on Middle East Economies

The impact of oil prices on Middle East economies is dictated by a volatile mix of external forces.

- Geopolitical Instability: OPEC+ fragmentation risks and conflict in key transit chokepoints like the Strait of Hormuz could trigger catastrophic price spikes or collapses.

- The Green Energy Transition: Exponential growth in renewables and EV adoption in Europe and China is permanently eroding long-term demand.

- Economic Power Shift: China’s economic slowdown is countered by rising demand from India and ASEAN, creating a fragile and unpredictable demand base.

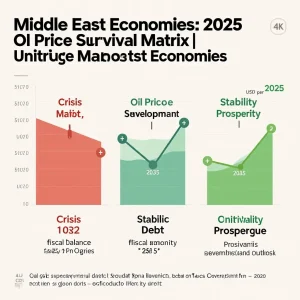

Analyzing the Impact of Oil Prices on Middle East Economies: 2025 Survival Matrix

This framework models the potential outcomes based on three Brent crude price scenarios for 2025.

| Economic Indicator | Crisis Scenario ($65-) | Stability Scenario ($80) | Prosperity Scenario ($95+) |

|---|---|---|---|

| Fiscal Balance | Deep Deficit (5-9% GDP) | Fragile Balance (±1.5% GDP) | Surplus (2-4% GDP) |

| Sovereign Debt | Explosive Growth | Managed Increase | Aggressive Paydown |

| Vision 2030 Progress | Stalled or Reversed | Slow, Pragmatic Advance | Accelerated but High Risk |

| Social Unrest Risk | Severe | Moderate | Low (Short-Term) |

| SWF Strategy | Capital Preservation | Balanced Growth | Aggressive Acquisition |

Framework Assumptions: Models a baseline of stable OPEC+ cohesion. Critical Limitation: A black swan event, such as a major regional war, renders all models obsolete.

Also read:UAE Visa-Free Entry

Strategic Responses to the Impact of Oil Prices on Middle East Economies

Scenario 1 – The Prosperity Illusion: Impact of High Oil Prices on Middle East Economies

False Security: Floods treasuries with cash, often incentivizing wasteful spending and delaying critical reforms, the ultimate long-term trap.

Unitribune Recommendation: Mandate that 70% of all surplus be funneled into non-oil GDP generating assets and sovereign wealth funds. Resist all political pressure to expand unsustainable public sectors.

Scenario 2 – The Tightrope: Moderate Oil Price Impact on Middle East Economies

The Most Dangerous Path: Fosters a false sense of security. This is the critical window to execute difficult reforms—privatization, subsidy removal, and bureaucratic overhaul—before the next crash.

Unitribune Recommendation: Implement means-tested social safety nets now to cushion the blow of future austerity. Double down on public-private partnerships for infrastructure.

Scenario 3 – The Abyss: Impact of Low Oil Prices on Middle East Economies

Brutal Reality: Exposes the utter failure of half-hearted diversification. Credit ratings plummet, capital flight accelerates, and social contracts fracture.

Unitribune Recommendation: Execute contingency plans for rapid asset monetization (e.g., NOC IPOs) and secure emergency credit lines. Prioritize spending on national security and critical imports above all else.

Understanding the Full Impact of Oil Prices on Middle East Economies: Action Plan

- Diversify or Die: Accelerate domestic value chains beyond crude—focus on petrochemicals, refined products, and green hydrogen for export.

- Leverage SWFs as Shields: Reposition Sovereign Wealth Funds from growth engines to defensive capital preservation tools during prolonged downturns.

- Embrace Radical Privatization: Sell stakes in national oil companies and state-owned utilities to raise capital and inject efficiency, irrespective of market sentiment.

- Secure Long-Term Contracts: Lock in Asian buyers with 10+ year supply agreements at fixed premiums to create revenue certainty.

For a deeper dive into Saudi Arabia’s specific risks, read our groundbreaking report on Saudi Vision 2030 Progress Amidst Oil Price Volatility.

For unparalleled data, reference the latest OPEC Monthly Oil Market Report.

Conclusion: Navigating the Impact of Oil Prices on Middle East Economies

The impact of oil prices on Middle East economies in 2025 will be a ruthless reveal of strategic preparedness. The time for gradual change is over. Nations that treat oil wealth as a permanent entitlement will face economic instability.

Unitribune’s Final Alert: Implement scenario-based stress testing immediately. Monitor IEA reports and global bond yields weekly. The future belongs to those who use oil not as a crutch, but as a finite resource to build a truly independent economy.

Also read:UAE Residency Visa Renewal Process

Frequently Asked Questions About the Impact of Oil Prices on Middle East Economies

Sovereign debt crisis. Nations like Bahrain and Oman, with high breakeven prices, could face insolvency without drastic spending cuts or bailouts from wealthier neighbors.

The UAE, particularly Dubai, built a diversified economy decades ago. Its non-oil sectors like tourism, aviation, and finance provide a critical revenue buffer that Saudi Arabia is still struggling to create.

Not in the foreseeable future. While projects like NEOM are strategic, their financial contribution is negligible compared to oil revenues. They are a long-term vision, not a near-term solution.

Approximately $78-$82 per barrel. This is the price needed to finance its current budget, including massive spending on Vision 2030 projects, without taking on new debt.

Diversify holdings across different GCC states, favoring those with lower breakeven prices (Qatar, UAE) and strong sovereign wealth funds. Avoid over-exposure to construction and contracting sectors during downturns.

2 thoughts on “Impact of Oil Prices on Middle East Economies: A 2025 Survival Guide”